(Image via abcnews.com)

Business Manager: Julian Cassady

Email: jcassady@umassd.edu

On March 10th, Silicon Valley Bank collapsed, leaving thousands of Americans unable to access their money.

So what happened?

To preface, Silicon Valley Bank (SVB) mainly serves the region of Southern California. Its customer base is mostly comprised of business owners of tech startups that receive a lot of private funding.

A string of fears over rising interest rates and a drought in venture capital investment has made these business owners and employees run to their respective banks to withdraw all of their liquid cash.

This is commonly referred to as a bank run.

Since many banks use depositor funds for borrowing and giving out loans, it usually isn’t possible for a bank to have enough cash on hand to allow everyone they service to withdraw all of their money.

A majority of these business owners and startup employees have a lot of money shored up in their SVB accounts.

Unfortunately, 94% of these accounts had more than the $250,000 maximum guaranteed to be insured by the Federal Deposit Insurance Corporation (FDIC).

This means that, in the case of a bank failure, most depositors at SVB would not be able to get their total account balances back through typical FDIC insurance.

Luckily, the Biden Administration has released statements that depositors at the collapsed banks like SVB will receive their funds in whole, without cost to the American taxpayer.

How do they plan on doing this?

The FDIC has a fund that all banks must contribute to yearly called the Depositor Insurance Fund (DIF). This is an additional emergency fund for bank failures such as these that the FDIC has total control over.

Investors who own Silicon Valley Bank stock will not be covered.

Their shares will be worthless as the government takes over and shuts down the company, delisting it from all stock exchanges.

The actions taken by the Federal Reserve Bank, the FDIC, and the Biden Administration prove that the government has learned from the financial crisis of 2008. Opting to kick investors to the curb to save the innocent customers of the collapsed banks and the economy at large.

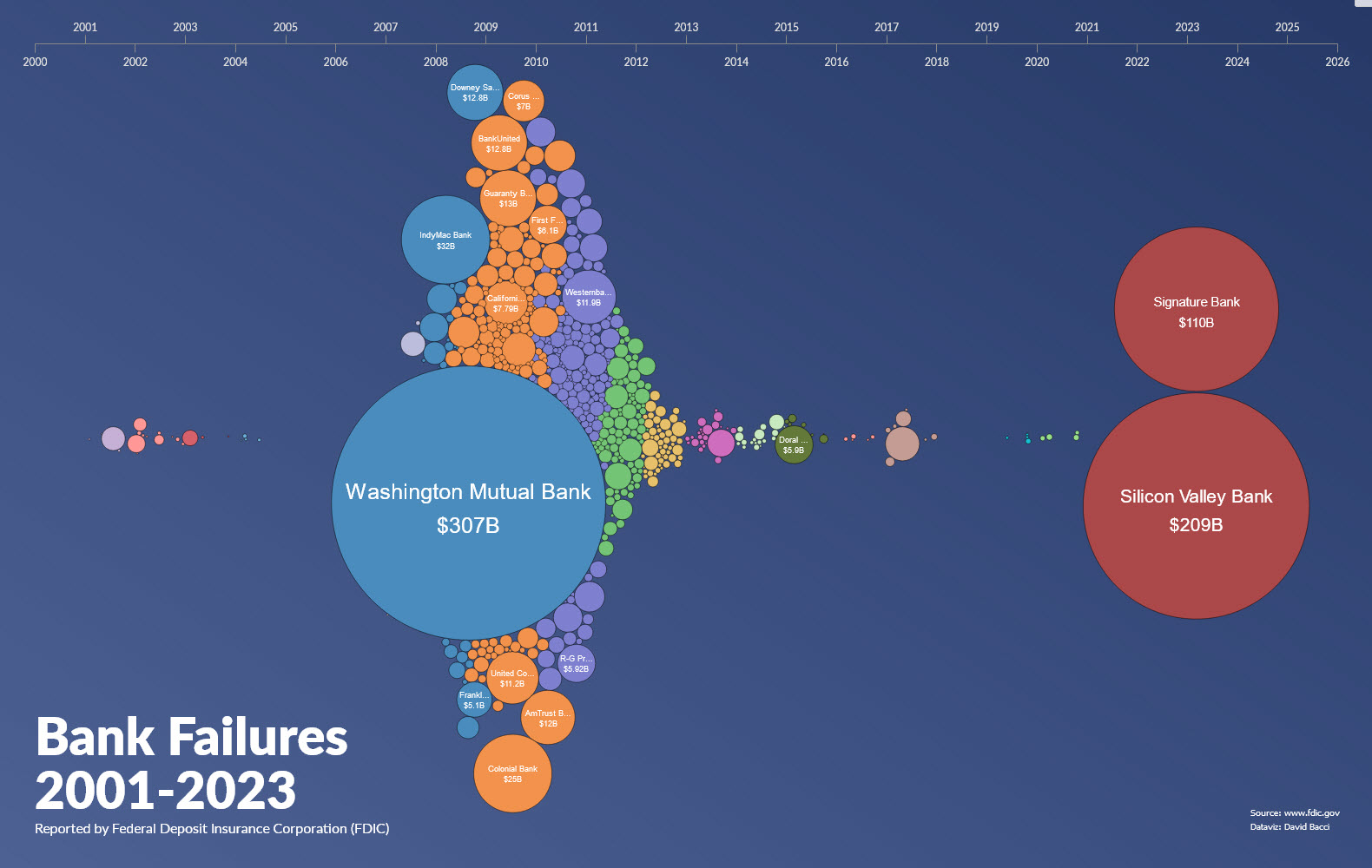

Shown above is a visual representation of the size of collapsed banks from the past couple of decades. It’s clear that today’s collapse trends look very different from 2007-2013.

One notable difference is that the bank collapses of the 08’ recession triggered a domino effect. Causing duplicate bank crashes to occur all over the world.

So far, the government has been able to contain the collapses within a few banks, which bear significant responsibility for failure.

Americans and economists are satisfied with the response towards the banks, especially because Silicon Valley and Signature Bank (another bank that failed recently) were heavily invested in cryptocurrency and other cryptocurrency-related investments.

It is important to note that cryptocurrency is popular mainly for its lack of regulation and decentralization.

People believe that banks who invest in unregulated and risky assets like cryptocurrencies should absolutely not be bailed out by taxpayer funding in the event of a collapse.

Between the risky bets in crypto and the tightening of the economy, banks are in for a rude awakening.

Economists and the Biden Administration alike are hoping that these moves don’t cause any more collapses like in 2008.

Only time will tell if supporting working class Americans ends up being the right thing for the economy.